A new secular growth begins

In our note Union Budget 2022 – What did it deliver?, we said that this was a transformative budget for India, harking back to the early 2000’s – the government was going to use the rising tax revenues to fund infrastructure projects rather than increasing subsidies, which it had previously done between 2014-19. In addition, the government had also come up with policy measures to boost local manufacturing – the production-linked incentive (PLIs) plans, which have given a fillip to private capex.

Further, as we have noted before, the Indian manufacturing sector is now operating at capacity utilisation of ~75-80% in practically all segments – thus, there is a major new private capex cycle starting, the first since the previous infra boom ended in 2011-12. During this period, Indian corporates have also significantly reduced their borrowings and cleaned up their balance sheets.

Therefore, we believe that we are the start of a multi-year cycle of new capex from both public and private sectors, which will act as a virtuous cycle for employment, wage growth and consumption. While the unexpected Russian attack on Ukraine has put some short-term hurdles (in the form of a sharp increase in oil prices), we are confident this is not a deal breaker for this theme.

In the following sub-sections, we look at specific segments of the economy and population benefiting from the Union Government policies, and the implications for Indian equity markets going ahead.

Public Sector Incentives

The Union Budget provided a whopping Rs7.5 lac cr investment outlay for FY22-23, a 35% yoy increase. Analysing this outlay further, we pick out the largest non-subsidy-based schemes, one each in Core Schemes and Major Central Schemes. The following table summarises the budgeted and revised estimates of expenditure on the Jal Jeevan Mission and National Highways Authority of India (NHAI) from the FY22-23 Union Budget publications.

| Scheme (Rs cr) | FY20-21 Actual | FY21-22 Budget Est | FY21-22 Revised Est | FY22-23 Budget Est |

| Jal Jeevan Mission | 10,998 | 50,011 | 45,011 | 60,000 |

| % of Core Schemes’ Expenditure | 5.5% | 17.6% | 15.3% | 17.5% |

| National Highways | 46,062 | 57,530 | 65,060 | 1,34,015 |

| % of Central Schemes’ Expenditure | 4.7% | 8.5% | 8.1% | 16.3% |

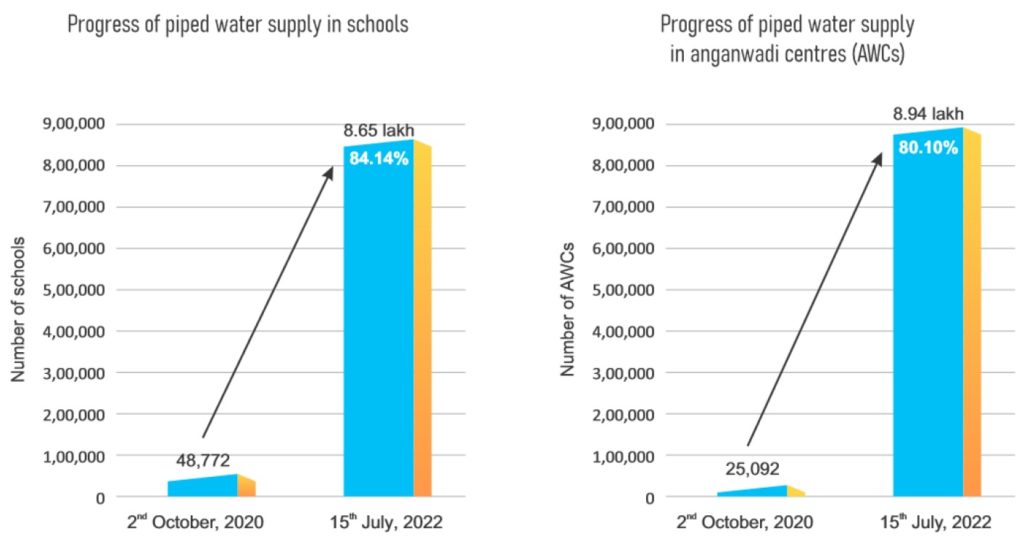

Jal Jeevan Mission (National Rural Drinking Water Mission)

In August 2019, only 17% of rural households had a Functional Household Tap Connection (FHTC)[1]. The FHTC penetration as of July 2022 stands at 51% (9.8cr households). Under the Jal Jeevan Mission (JJM), the need for water supply also extends to schools and anganwadi (childcare) centres.

While states like Goa, Telangana and even Gujarat have been beneficiaries of this overall growth, Northern states like UP, Jharkhand, and Chhattisgarh are still severely under-penetrated. Interestingly, the Embassy of Denmark has partnered with the United Nations Office for Project Services for tap water access in Mirzapur.

The push is largely beneficial from a hygiene and nutrition perspective. For example, the JJM publication cited research that claims that inadequate sanitation standards are a cause for dropout rates for pubescent women in school. The applications of sanitary water are not just limited to hygiene, but also to the overall development of children in rural areas from cooking to cleanliness. An economist at JJM also proved via unit economics (though with some strict assumptions and arguably unquantifiable opportunity costs/benefits in practice) that there is an 8x benefit-to-cost ratio of providing 275 litres a day to a 5-member household.

The ever-increasing budget allocation to this scheme is sending a clear message that the Central Government is determined to improve rural livelihood at the most essential level of Maslow’s hierarchy of needs. The trend in published data shows that there is support of this goal thus far. Besides irrigation pipelines and related facilities, quality construction of check dams is a must for sustainable access to water. In this context, availability of quality labour and construction design needs to be in place, especially for states in which heavy rains can wash away the plans of the JJM.

National Highways

The FY23E Union Budget proposed an additional 25,000km of national highway expansion. To put this in context, Crisil estimates that the total highway construction was 10,457km in FY22. Further, the absolute amount allocated to highways in FY23E is double that of the previous year’s estimated actual spend. As it stands, supply chain issues and high input prices have led to relatively lower daily average construction, but this is expected to pick up after monsoon.

From cement to capital goods, there are several sectors that stand to gain from the push for highway expansion. The Prime Minister launched projects worth Rs27,000cr in Bangalore and Rs31,500cr in Tamil Nadu in June itself. This includes the 258km Bangalore-Chennai expressway. Inter-state connectivity and ease of freight transport are vital to the underlying growth of the economy. For instance, Ashok Leyland reported that their Medium and Heavy Commercial Vehicle sales increased 238% yoy in June 2022. This is very exciting as this indicates industrial and transport demand is picking up after a lull of many years – and, this also creates a virtuous cycle of further demand generation in the supply chain for trucks, and increasing employment for drivers / driver-owners.

Private Sector Incentives

Since 2020, the government’s policy push for Aatmanirbhar Bharat has created several PLIs to incentivise a wide range of manufacturing sectors in India. We have taken a select few incentives (as classified by the National Investment Promotion & Facilitation Agency[2]) as a proxy for encouragement of private capex in India.

Automobile and Ancillary

The Ministry of Heavy Industries (MHI) reported that the Auto and Auto Components PLI Scheme has received a proposed investment of Rs74,850cr against an anticipated proposal of Rs42,500cr, to be spent over a span of five years, starting April 2022. The key focus in this segment is to attract investment in Advanced Automotive Technology (AAT) in “overcoming cost disabilities, creating economies of scale and building a robust supply chain”[3]. There are a handful of Indian subsidiaries of foreign players that also stand to benefit from this scheme.

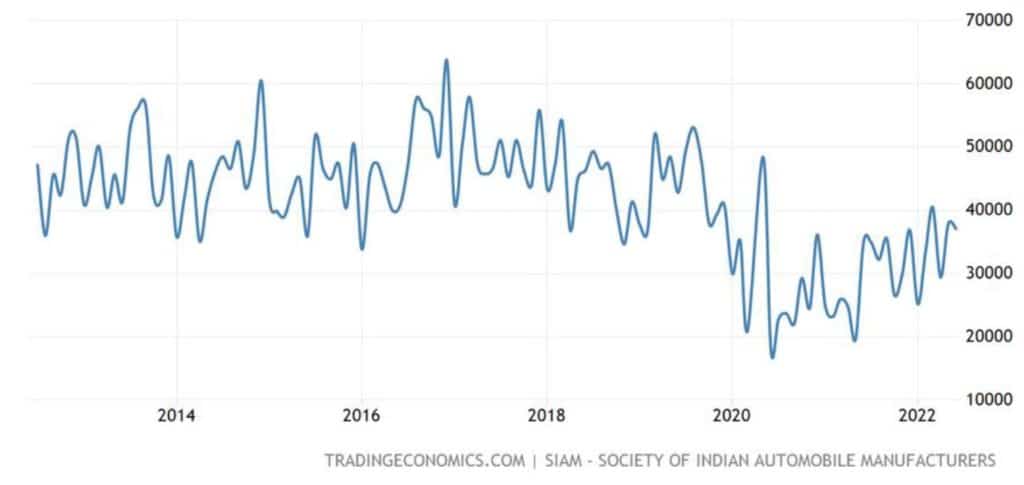

If the priority of cost optimisation is implemented as expected, it could potentially make exports more competitive. Data from the Society of Indian Automobile Manufacturers (“SIAM”) shows that Passenger Vehicle export volumes fell 23.8% over FY17 to FY22 while Two-Wheeler export volumes more than doubled over the same period. However, Passenger Vehicle exports are on an uptrend since 2021 with some monthly variation, showing signs of recovery.

The key reason that we consider this to be important – Automobile manufacturing and related ancillary supply chains account for ~50% of India’s manufacturing base. Thus, any increase in demand for autos, whether domestic or global, is a key driver for the Indian economy. The markets have taken note, and the NSE Auto Index is up 16.5% YTD, the best performing sectoral index so far, this year.

Indian Exports of Passenger Vehicles (volume in units)

Further, the success of foreign auto companies in India is largely determined by the cost-conscious Indian consumer. In a best-case scenario, apt implementation of incentivising cost reductions can encourage operational efficiency, which could reverse the phenomenon of foreign-owned factories shutting down (eg: Ford and Harley Davidson).

Chemicals

Creating synergies with the PLI policy for autos, the MHI’s PLI policy for chemicals benefits companies investing in creating supply chains for Advanced Chemistry Cell (ACC) for Battery Storage. The outlay of Rs18,100cr is expected to be spent over five years to increase the manufacturing capacity of ACC Battery Storage by 50GWh – the capacity demand was oversubscribed 2.6x. The key beneficiaries are largely in the renewable energy and EV segments.

The small but growing EV space has gained ground under the FAME India Scheme – the MHI has been sanctioned Rs1,000cr under Phase 2 of the scheme for EV infrastructure. There are many ancillary benefits of the PLI for ACCs. For example, it encourages backward integration into building infrastructure for battery manufacturing itself, and so chemicals-related services will also get a boost. Additionally, the big bet on EV then trickles into creating efficiencies in the power grid, where some power companies will see a benefit. It also encourages India to keep up with global EV and hybrid vehicle trends, the success of which will be highly dependent on the cost effectiveness to the end consumer.

Electronics Manufacturing

Another top expenditure in the PLI schemes, the Ministry of Electronics and Information Technology (“MEITY”) has been allocated Rs40,951cr for electronics manufacturing and Rs7,235cr for IT hardware. This is a key policy initiative targeted at global manufacturers looking at China-plus-one. The Indian government hopes that it can create an electronics manufacturing ecosystem to parallel the large engineering and manufacturing ecosystem that India already has in automobiles. While we have already seen global EMS companies invest in mobile phone assembly and some manufacturing, the key success of this scheme will depend on whether we can get to semiconductor manufacturing companies to set up shop in India.

Further, the government is actually trying to improve efficiencies in delivery of government services by bringing more citizens into the “e-Governance” net by “enhancing efficiency through digital services and ensuring a secure cyber space”[4]. For instance, data from MEITY shows that the cumulative Registered Beneficiaries under the Digital Literacy Scheme has increased from 6.0lacs to 6.12cr over April 2017 to June 2022 (with a sharp monthly surge from November 2020 onwards). Another important KPI tracked by MEITY is the number of Digital Payments – monthly BHIM UPI transactions have increased 590% over April 2019 to June 2022, with a steady uptrend.

This can help further formalisation of the Indian economy and have positive benefits for labour productivity. Additionally, digitization of rural financial savings is particularly beneficial to the Indian financial services sector (particularly MSME finance) and fintech-related software services.

Textiles

Textiles has been a prominent industry in terms of manufacturing value and employment[5], and was previously one of India’s premier manufacturing sectors before losing out to China, and even Bangladesh, Sri Lanka and Vietnam. In this context, the PLI for textiles is largely export-oriented with a push for incubators, including manufacturing support and skill development. A proposed outlay of Rs10,683cr has been approved for 61 out of 67 applicants, across brownfield and greenfield investments.

While the PLI scheme provides long-term benefits, the industry has been facing some short-term headwinds. Cotton prices increased almost 77% over Aug 2021 to May 2022. To ease input costs and to deal with a shortage of domestic cotton, the Government has also extended a waiver of customs duty for cotton until Oct 2022. Although prices have now come down by 35% since peak, demand for apparel has also been shrinking due to a slowdown in the US – in our July 2022 Update we mentioned that US retail chains are focusing less on discretionary items and more on staples – this includes over supply / inventory build-up in the apparels segment. On the other hand, it is also important to note that China’s share of textile exports has shrunk in 2022, largely due to a US ban.

Vietnam has been able to capitalise on this trend, and it is now an opportune moment for India to follow suit. While the growth story may take time to materialise, it is likely to bring with it momentum in employment and export competitiveness.

Summary

The Union Budget proposals and the PLI schemes are providing one of the largest tax-payer funded support for capital expenditure, both public and private, that we have seen in the history of independent India.

On public expenditure, the JJM and NHAI proposals are extremely positive on account of rural livelihood improvement, rural health and quality of life improvements and cross-country connectivity.

On the private side, promotion of the captioned industries will have a direct impact on employment generation, and hence sustained consumption demand, leading to the creation of a virtuous, self-sustaining economic cycle. It may also attract FDI once there is proof of concept that India’s Ease of Doing Business is actually improving on the ground.

Although equities have been volatile through 2022, primarily due to rising inflation and the consequent increasing interest rates regime, we believe that the current government policies are setting a base for creating a global manufacturing and supply chain base in India – this will lead to sustained economic performance over the next decade, and the stock market typically discounts future cash flows to the present! Thus, we think that the current equity market volatility is giving investors an opportunity to create a solid base for future sustained gains from equities.

Disclaimer

The data, tables, graphs, and all other depictions are provided by Accord Fintech Private Limited, unless mentioned otherwise on or below the depiction. ATREYI FINANCIAL SERVICES PRIVATE LIMITED is not liable or accountable for accuracy of the data provided in this Document.

This document is provided for informational purposes only and it is for the intended recipients only as transmitted by way of printed, electronic, or other media and is not intended as an offer to sell or solicitation of an offer to buy securities or other instruments.

The information contained herein is based on our assumptions, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us, or which was otherwise reviewed by us and can be changed without any prior intimation. This information must not alone be taken as the basis for an investment decision. Please consult your financial, legal and/or tax advisors.

Investment in securities is risky and there is no assurance of returns or preservation of capital. Neither ATREYI FINANCIAL SERVICES PRIVATE LIMITED, nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost capital, lost revenue or lost profits that may arise from or in connection with the use of this information.

Any investment in any product described in this Presentation will be accepted solely on the basis of the offering entity’s constitutional documents, accordingly, this presentation will not form the basis of, and should not be relied upon in connection with any subsequent investment in the fund/ security.

ATREYI FINANCIAL SERVICES PRIVATE LIMITED does not accept any responsibility for any errors whether caused by negligence or otherwise or for any loss or damage incurred by anyone in reliance on anything set out in this Document.

Any person/s accessing data contained in this presentation, hereby confirms that they are not a U.S. person, in accordance with the definition of the term “US Person” under relevant US Securities laws.

No part of this material may be copied or duplicated or redistributed without prior written consent.

Mutual Funds are subject to Market Risks; please invest after seeing the Offer Documents.

[1] Jal Jeevan Mission Publication

[2] National Investment Promotion & Facilitation Agency

[3] Press release by Ministry of Heavy Industries (March 2022)