Earnings and FIIs drive markets in July

Banking and FMCG stocks gained the most in July, while IT stocks started to show some strength despite reporting weak margins for 1Q. Besides liquidity and interest rate expectations, Indian equity markets were driven by earnings data in July. Overall, 1Q FY23 earnings have been largely supportive of our fundamental thesis for the Indian economy.

| Index | Monthly Returns | YTD Returns | Returns from 52-wk highs |

| NIFTY 50 | 8.6% | -2.7% | -7.8% |

| NIFTY MIDCAP 100 | 11.1% | -3.7% | -10.9% |

| NIFTY SMALLCAP 100 | 8.1% | -19.7% | -23.9% |

| NIFTY BANK | 12.7% | 2.9% | -10.4% |

| NIFTY AUTO | 5.8% | 12.9% | -1.2% |

| NIFTY FMCG | 12.7% | 13.0% | -0.2% |

| NIFTY IT | 3.6% | -25.5% | -26.1% |

| NIFTY MEDIA | 9.4% | -7.6% | -16.7% |

| NIFTY METAL | 15.4% | -2.5% | -19.6% |

| NIFTY PHARMA | 4.6% | -9.7% | -14.5% |

| NIFTY REALTY | 15.6% | -7.9% | -19.6% |

Earnings season kicked off with the IT sector – TCS and HCL both reported mid-teens yoy revenue growth, on a constant currency basis, but operating margins contracted on a quarterly basis again. This was due to continuing higher salary costs and attrition for the industry. This could likely persist for the rest of 2022 for Indian IT services – although, we are seeing softening hiring trends for Big Tech in the USA. IT stocks’ performance can be a drag on domestic large cap indices, as the IT sector was 16% to the free float market cap of Nifty 50 as of June 30th.

Infosys surprised the market by stronger than expected revenue growth and increased its revenue guidance for the full year. However, it also reported significant margin pressure. On the other hand, Tata Elxsi and L&T Technology Services reported expansion in operating margins, led by their focus on digital and technology solutions for industrial companies.

ICICI Bank’s results showed an encouraging sign of underlying credit growth – retail yoy growth stood at 24.4% (5.1% qoq), while their domestic corporate portfolio grew by 14.4% yoy (4.4% qoq), with an increasing share of higher quality borrowers. However, Axis Bank’s corporate loan book shrunk 5% yoy, despite beating bottom-line expectations. The rising rate scenario coupled with retail credit growth has helped improve net interest margins for the banking heavyweights – the Nifty Bank index was a top performer in July, although it has been volatile since start of the year.

The infrastructure theme continues to be strong with UltraTech Cement beating expectations and L&T reporting strong order flow. However, at a granular level, profitability of cement products on a per tonne basis has been hit due to rising energy costs. Volume growth is encouraging, but the industry faces the challenge of potential oversupply, given the planned capex reported by cement companies. So, even when supply-related inflation eases, demand-side factors will dominate the narrative.

Steel companies have already witnessed a similar phenomenon but due to different reasons. For instance, JSW Steel has reported 93% capacity utilisation of existing plants as of 1Q FY23 while revenues have shrunk by 14% qoq, both on a standalone basis. Similarly, Jindal Steel’s 1Q FY23 numbers highlighted that Indian steel consumption grew at a marginally lower rate than Indian steel production. While India stands to gain on China’s production cuts, slowing growth in the global economy still poses some challenges from a demand perspective.

The quarterly numbers of major auto companies either met or beat analyst estimates for the most part – the volume numbers for July are also showing a rising trend. The only soft part in this sector remains the 2W segment, but even here we are starting to see better volume numbers.

In retail, D-Mart reported a blow-out quarter, partially thanks to inflation increasing price points, which helped margins and higher footfalls across their stores. FMCG companies also reported margin expansions and volume growth across practically all product categories. HUL reported a significant volume increased after over 10 quarters.

The quarterly numbers have been very supportive of our thesis that private capex led spending is driving demand for goods and employment across the country, which in turn leads to increased consumption and demand for goods and services. While some part of the better-than-expected revenue increases can be attributed to inflationary price increases, we are also seeing strong and consistent volume growth in 2022. With commodity prices becoming more favourable now, corporates will have better support for margins for the rest of the year – as we have rarely seen consumer price cuts, once inflation moderates. This will support earnings growth for domestic consumption companies. Infra and capex related companies should also benefit from moderating commodity prices, from a volume growth perspective, even if they do not hold on to pricing increases.

As per Deloitte’s India Economic Outlook[1], India is pegged to remain one of the fastest growing global economies. According to their research, 70% of India’s economy is driven by consumption and investment. Additionally, strong tax revenues and the proposed government capital expenditures that will follow can further propel the India growth story. Therefore, a prolonged multiplier effect can follow once the current global scenario becomes more positive.

The risk of global demand destruction remains due to the rising rate environment – however, this can positively affect India’s balance of trade in the short to medium term if commodity prices remain lower for longer (see our previous monthly note). We export gems and jewellery, engineering products and IT services – these are not affected by commodity prices going down, but our import bill goes down and input prices for engineering exports goes down making them more competitive.

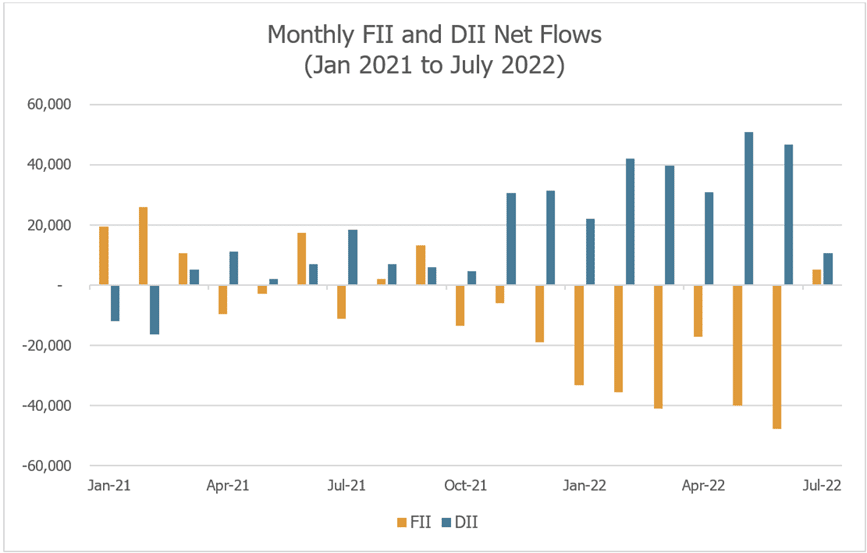

FIIs and DIIs in sync for the first time in 2022

DII net buying in Indian equity markets continued, despite a cool-off in July 2022. However, FIIs turned net buyers of Indian equities on a monthly basis for the first time since September 2021. This data is particularly encouraging from an emerging markets perspective. The Shanghai Composite index was down by 3.4% in July while Taiwanese and South Korean indices remained relatively flat. The Nifty 50 index has delivered significant alpha over these indices, indicating that India can potentially be a top performer in Asian markets when emerging market sentiment strengthens.

Further, FDI inflows were above Rs6.0 lac crore for FY21-22. Rs1.68 lac crore of this amount is attributed to the manufacturing sector, which saw a 76% yoy growth in funding. This is supportive of the overall India growth story in which domestic manufacturing stands to gain.

A Global Roundup of Important Events

The spotlight this month from the Russia-Ukraine war was on the hunger crisis that it has caused. A drought in East Africa and restricted grain exports from Ukraine has wreaked havoc. A report by World Food Program mentioned that 90% of East Africa’s wheat is imported from Ukraine. A similar situation persists in Yemen, which depends on Ukraine for 30% of its wheat consumption.

Meanwhile, EU energy ministers approved steps to reduce natural gas demand / consumption by 15%. This move was aimed to safeguard European citizens from a heating crisis in the upcoming winter months. The French government nationalised its energy behemoth, Électricité de France, due to the company’s inability to pay its massive debt and operating costs. French authorities are also considering joining the energy windfall tax bandwagon – its largest oil and gas company, Total, reported that its 2Q profits tripled on a yoy basis.

The Italian 10-year bond yield spread versus the German Bund spiked on Mario Draghi’s resignation and it is still trading at a 3-yr high. This is increasingly worrying since Italy’s debt-to-GDP ratio was above 150%, as of March 2022, compared with the Eurozone average of 95.6%. The ECB raised interest rates from zero to 0.5% for the first time in 11 years, further aggravating Italy’s debt woes.

Global financial markets remained range bound in anticipation of the July FED rate hike and its subsequent commentary. The FED hiked rates by 75 bps for the second time in a row to 2.5%, but the US markets were buoyant because they expect the FED to stop hiking rates sooner than later now, and to start cutting rates in 2023. The FED said that the pace of rate hikes will be determined on a “meeting-to-meeting” basis, based on economic data released between its meetings – the market took this to mean that the FED will stop increasing rates soon.

We note that US M2 money supply has increased 36% from March 2020 to January 2022, causing a lot of the asset price inflation that we have seen so far. In turn, just the start of monetary tightening has caused asset price deflation in 2022. Energy price inflation coupled with supply chain disruption has caused some demand destruction at the consumer level, thereby slowing down the US GDP growth rate.

US unemployment stood at 3.6%, as of June, and hiring in manufacturing has not slowed down drastically on a yoy basis. This is the paradox for US markets right now – if the FED considers this full employment and inflation numbers show no sign of coming down, it will continue raising rates, thereby, increasing the risks for a deeper recession down the line. And, if the markets continue to rally because it expects QT to come to an end before it has even properly begun, then also the FED has no incentive to stop raising rates and continuing with QT.

Ekam Recommendations

We urge investors to remain cautious about the current “risk-on” rally in the equities market – to us, this seems like a bear market rally in the US, leading to risk-on trades in other markets, rather than the start of a true, new bull market rally in the US. Therefore, while we remain constructive on Indian equities, and believe that 2022 is going to be an excellent base year for the next bull market in Indian equities, investors should continue to expect pull backs this year.

It is important to remain invested with Portfolio Management Services that have a track record of weathering market volatility and coming out of it stronger. Additionally, we remain positive on the Dividend Yield space as far as equity mutual funds go.

Exposure to debt should only be taken via direct investments in high-quality bonds rather than debt mutual funds and held to maturity to avoid mark-to-market losses.

We retain our view that gold should remain in the 10-20% range of an investor’s portfolio, as it has continued to be a hedge against equity market volatility and rupee depreciation. In fact, gold prices have dropped by 5.5% in US$ terms YTD but the US Dollar itself is at historical highs against all other major currencies due to a flight to safety. This left gold prices relatively flat YTD in INR terms, outperforming both equity and bond returns.

Disclaimer

The data, tables, graphs, and all other depictions are provided by Accord Fintech Private Limited, unless mentioned otherwise on or below the depiction. ATREYI FINANCIAL SERVICES PRIVATE LIMITED is not liable or accountable for accuracy of the data provided in this Document.

This document is provided for informational purposes only and it is for the intended recipients only as transmitted by way of printed, electronic, or other media and is not intended as an offer to sell or solicitation of an offer to buy securities or other instruments.

The information contained herein is based on our assumptions, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us, or which was otherwise reviewed by us and can be changed without any prior intimation. This information must not alone be taken as the basis for an investment decision. Please consult your financial, legal and/or tax advisors.

Investment in securities is risky and there is no assurance of returns or preservation of capital. Neither ATREYI FINANCIAL SERVICES PRIVATE LIMITED, nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost capital, lost revenue or lost profits that may arise from or in connection with the use of this information.

Any investment in any product described in this Presentation will be accepted solely on the basis of the offering entity’s constitutional documents, accordingly, this presentation will not form the basis of, and should not be relied upon in connection with any subsequent investment in the fund/ security.

ATREYI FINANCIAL SERVICES PRIVATE LIMITED does not accept any responsibility for any errors whether caused by negligence or otherwise or for any loss or damage incurred by anyone in reliance on anything set out in this Document.

Any person/s accessing data contained in this presentation, hereby confirms that they are not a U.S. person, in accordance with the definition of the term “US Person” under relevant US Securities laws.

No part of this material may be copied or duplicated or redistributed without prior written consent.

Mutual Funds are subject to Market Risks; please invest after seeing the Offer Documents.