Upbeat domestic markets in August

Indian equities have traded in a narrow upward channel since the start of August, without a clear catalyst for bulls or bears. Small caps joined the uptrend this month, but Nifty IT continues to be battered. All the other major sectoral indices posted steady, positive gains.

| Index | Monthly Return | YTD Return | Return Since 52-wk high |

| NIFTY 50 | 3.5% | 2.3% | -4.5% |

| NIFTY MIDCAP 100 | 6.2% | 3.4% | -5.3% |

| NIFTY SMALLCAP 100 | 4.9% | -14.8% | -20.1% |

| NIFTY BANK | 5.5% | 11.4% | -5.5% |

| NIFTY AUTO | 5.4% | 20.9% | -1.2% |

| NIFTY FMCG | 3.1% | 16.6% | -0.1% |

| NIFTY IT | -2.6% | -26.6% | -28.0% |

| NIFTY MEDIA | -0.5% | -6.7% | -17.1% |

| NIFTY METAL | 8.2% | 7.5% | -13.1% |

| NIFTY PHARMA | -0.6% | -1.1% | -15.0% |

| NIFTY REALTY | 2.7% | -4.3% | -17.4% |

Crude oil prices have come off ~25% since June and this reduced the pressure on India’s trade deficit to some extent. But the US Dollar Index breached a 5-year high yet again, as the Rupee touched a monthly low of Rs80.13/USD, increasing pressure on imports. A slowdown in the global economy, thanks to the Russia – Ukraine war, has also put pressure on exports, leaving the trade balance relatively lower than July levels. Provisional data shows that exports shrunk by 1.2% yoy in August, marking the first contraction since February 2021. Indian manufacturers do stand to gain as commodity prices cool off, but lack of global demand may keep earnings growth subdued for this quarter.

These effects can be seen in 1Q FY23 India GDP – GDP growth came in at 13.5% yoy, but this was significantly lower than RBI’s estimate of 16.2%[1]. Subdued private and government consumption have caused a drag despite strong capital expenditures from Central and State Governments. We are not yet seeing the capex spending translating into higher rural spending. Additionally, rural inflation has surpassed urban inflation, which has also depressed consumption demand of a key segment of India’s private consumption story. Unfavourable weather conditions have disrupted crop harvesting, potentially leading to a dampened festive season.

Monthly GST collections dipped slightly to Rs1.43lac crore for July, but it still continues a six-month trend line of GST revenues above Rs1.40lac crore. A large part of these strong collections could be attributed to greater formalisation of India’s economy and higher price levels. If this be the case, GST collections have proven to be a robust source of Government revenue, and this is positive for India’s fiscal deficit.

Total tax revenues for 1Q FY23 increased 15% yoy, while expenses increased only 13% yoy. Fiscal deficit for 1Q FY23 was 20% of FY23BE – we note that the Federal Government’s fiscal management has improved significantly in recent times, and the Finance Ministry has been nimble with many of its fiscal measures.

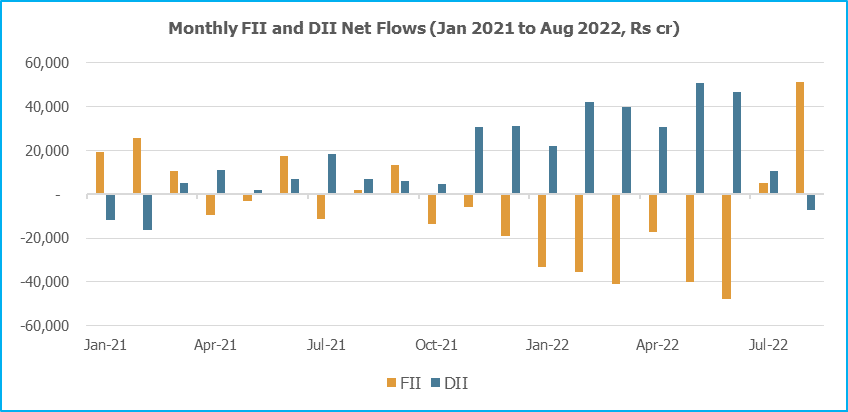

FIIs return to Indian equities

FIIs returned in August with a big bang, net buyers of Indian equities worth Rs51,241cr, while DIIs were minor net sellers. So far, this year, FIIs and DIIs have been net buyers together only in July.

Although the Nifty and Sensex faced clear resistance as they approached previous highs, the downside volatility remained relatively subdued towards the end of the month – the two indices bounced back after a 4% drop since the month’s peak, ending the month on a positive note. While we cannot affirm with certainty that Indian equity markets have bottomed out, the sudden spurt of FII investing has kept markets upbeat.

It should be noted that these purchases have been made during a global liquidity-tightening regime and a strengthening US Dollar. As the FED continues increasing rates and reducing its balance sheet, we expect pullbacks in the US markets, which could then lead to some pullbacks in the Indian markets over the next couple of months. But, given that India is the only large economy that is growing, while rest of the large economies, including China, face contraction or recession, it will continue to attract investment flows in the future. Further, we strongly believe that 2022 will come to be seen as the base year for multi-year growth in the Indian economy.

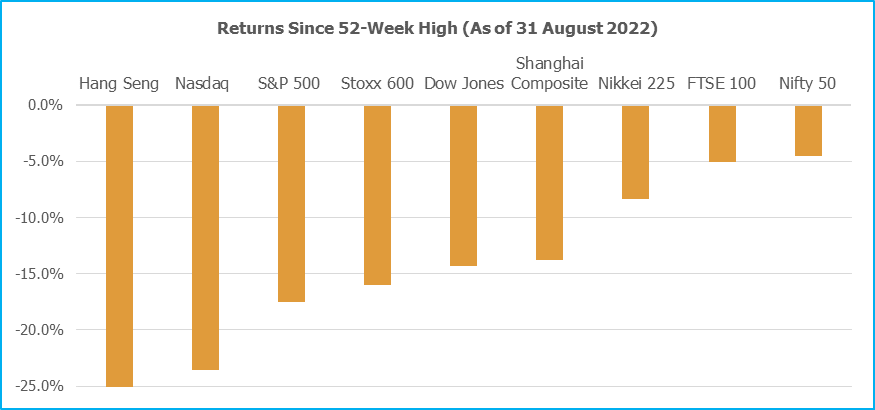

Indian equity markets in a global context

Most global indices breached the -20% mark since peak (a generalised definition of a bear market), but some like the Nikkei 225 and FTSE 100 have bounced back. The Nifty 50, too, has performed extremely well in this context. Indian equity markets have consistently outperformed international markets since the start of the year, especially during periods of sudden risk-off behaviour, which sends global markets on a down leg.

East Asian economies have been showing weakness since the start of the year. For instance, Hong Kong’s quarterly GDP growth came in at 1.0% for 2Q CY23 and -2.9% before that. Similarly, China logged a -2.6% decline for 2Q CY23, missing analyst estimates. This prompted Chinese authorities to cut interest rates when the entire world is following monetary tightening. A slowdown in China can turn out to be beneficial for India as it has been the large consumer of commodities globally – weak commodity prices are net beneficial to India, as India is a net consumer of commodities.

In the USA, Jerome Powell’s commentary at Jackson Hole was a key driver of a selloff in US equities at the end of the month. In his speech at the annual symposium, the FED Chief reiterated very strongly that price stability will remain its key priority despite causing “some pain” to households and corporations.

Indeed, the US consumer is already witnessing this pain as the 30-year fixed mortgage rate inched past 6% yet again this year after Powell’s hawkish comments. This is likely to discourage new homebuyers, further aggravating the woes of a broad-based oversupply in the US housing market. According to the National Association of Homebuilders, Residential Fixed Investments and Housing Services contributed ~16% to US GDP. Therefore, a prolonged slowdown in housing and housing-related activities is conducive to Powell’s agenda of price stability.

On the other hand, a more forward-looking survey conducted by the Conference Board, a private research group, indicated that US Consumer Confidence has rebounded in August, largely due to a positive short-term outlook on economic conditions.

Europe continues to be plagued by an energy crisis as the Nord Stream 1 pipeline’s allegedly unattended maintenance issues have sent natural gas prices back to elevated levels. The disruption to supply is poorly timed due to the onset of a cold European winter as gas distributors will pass on the increased wholesale price to retail consumers. For instance, natural gas prices in the UK have risen by 65% since July, despite their relative lack of dependence on Russian gas.

While EU countries have been urging their citizens to cut gas consumption by 15%, the increase in price may offset any benefit of lower consumption, leaving the average European citizen worse off. This has further encouraged German authorities to keep two out of its three nuclear power sources as a last resort to meet any shortfall in energy demand.

In this context, India has been doing relatively better, both from a fundamental perspective and from an equity markets perspective. It has become apparent that even during drawdowns, foreign money is being pushed into Indian equities. This is a validation of the long-term India growth story despite some blips in the near term.

Atreyi Recommendations

Investors should always keep in mind that bear markets can have significant short-run bull rallies. The latest risk-on rally in the US markets was probably caused by the market misreading previous comments by the FED Chair that future interest rate increases will be based on incremental economic data – the market took this to believe that most of the rate increases have been done, and the FED will start cutting rates in 2023!

However, the Jackson Hole commentary from Powell threw cold water on this thesis – and, we saw how quickly US sentiment changed. Powell recognises that the credibility of the FED as an institution itself is at stake, if it is not able to bring inflation under control, which was its primary core mandate, until enabling “full employment” was also added as a twin mandate. We believe that returning to a neutral rate means that the FED will keep pushing on rates for longer than most people expect, even if that means a limited, deeper recession in the US.

We believe that the last leg of 2022 will remain a period of consolidation in equity markets. Hence, we continue to recommend keeping equity investments limited to Fund Managers that have demonstrated previous success in navigating market volatility. It is also a good time to look at equity-oriented Mutual Fund schemes that can provide stability during volatile times, like Dividend Yield funds.

We are still not recommending investments in Debt Mutual funds, due to interest rate volatility. Instead, it is best to remain invested in direct bonds with fixed coupons, with low tenure.

For more conservative investors, Gold remains a solid asset class as a buffer to downside volatility. There should be a 10-20% allocation of the yellow metal in an investor’s portfolio, with more conservative investors on the higher end of allocation.

Disclaimer

The data, tables, graphs, and all other depictions are provided by Accord Fintech Private Limited, unless mentioned otherwise on or below the depiction. ATREYI FINANCIAL SERVICES PRIVATE LIMTED is not liable or accountable for accuracy of the data provided in this document.

This document is provided for informational purposes only and it is for the intended recipients only as transmitted by way of printed, electronic, or other media and is not intended as an offer to sell or solicitation of an offer to buy securities or other instruments.

The information contained herein is based on our assumptions, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us, or which was otherwise reviewed by us and can be changed without any prior intimation. This information must not alone be taken as the basis for an investment decision. Please consult your financial, legal and/or tax advisors.

Investment in securities is risky and there is no assurance of returns or preservation of capital. Neither ATREYI FINANCIAL SERVICES PRIVATE LIMITED, nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost capital, lost revenue or lost profits that may arise from or in connection with the use of this information.

Any investment in any product described in this Presentation will be accepted solely on the basis of the offering entity’s constitutional documents, accordingly, this presentation will not form the basis of, and should not be relied upon in connection with any subsequent investment in the fund/ security.

ATREYI FINANCIAL SERVICES PRIVATE LIMITED does not accept any responsibility for any errors whether caused by negligence or otherwise or for any loss or damage incurred by anyone in reliance on anything set out in this Document.

Any person/s accessing data contained in this presentation, hereby confirms that they are not a U.S. person, in accordance with the definition of the term “US Person” under relevant US Securities laws.

No part of this material may be copied or duplicated or redistributed without prior written consent.

Mutual Funds are subject to Market Risks; please invest after seeing the Offer Documents.