Markets take a toss in June, globally

Indian equities faced the brunt of the selloff in emerging markets as all indices except Auto ended the month in the red. FMCG and Autos have fared relatively well since their 52-week peak levels, but IT – a sector that we had originally anticipated to do well this year – has been hammered on FII selling. According to a recent report, 93% of FII selling has been concentrated in IT and Banks. Metals have also cooled off, in tandem with the falling commodity prices as a result of global demand destruction.

India’s economy continues to show resilience as shown by GST collections of Rs1.44 lac crores for May 2022. This marks an entire year of monthly collections above Rs1.4 lac crores. Further, as of June 16, net direct tax collections for FY22-23 stood at Rs3.39 lac crores (up 45% yoy), which includes Corporate Income Taxes of Rs1.71 lac crores. This is encouraging, given that the Finance Ministry had estimated revenues of Rs7.2 lac crores from Corporate Taxes, and a Net Tax Revenue of Rs19.35 lac crores in the FY23 Union Budget.

On the other hand, there are several fiscal measures that have been taken since June to bring some respite to soaring input prices. Two key policies include excise duty cuts on petrol and diesel by Rs8/litre and Rs6/litre, respectively, and the increase of fertiliser subsidy by Rs1.1 lac crores. To counter the Centre’s revenue hit from the cut in excise duty, the Finance Ministry subsequently hiked the export duty on petrol and diesel and also imposed a windfall tax on oil producers in the form of a special additional excise duty. Shares of Reliance and ONGC fell by 7% and 12%, respectively, on this announcement.

While 4Q FY22 earnings have been encouraging despite last-minute uncertainty, it will be important to track if sectors like Auto and FMCG can continue to perform on a fundamental level. Further, a reversal in the IT sector may be possible after there is evidence of better margin quality. We are also witnessing rising M&A activity in the Pharma sector: JB Pharma acquired four paediatric brands of Dr. Reddy’s, signalling confidence of growth in this space. This marks JB Pharma’s third acquisition in FY23. Subsequently, Dr. Reddy’s has acquired a range of generic injectable products from US-based Eton Pharmaceuticals for US$5 million in cash plus US$45 million in contingent payments. There have been some other smaller acquisitions in the sector, too.

| Index | Monthly Return | YTD Return | Return Since 52-wk high |

| NIFTY 50 | -4.9% | -9.1% | -15.2% |

| NIFTY MIDCAP 100 | -6.5% | -13.1% | -20.4% |

| NIFTY SMALLCAP 100 | -8.3% | -25.2% | -29.9% |

| NIFTY BANK | -5.8% | -5.8% | -20.1% |

| NIFTY AUTO | 1.0% | 7.0% | -3.6% |

| NIFTY FMCG | -2.7% | 0.2% | -10.4% |

| NIFTY IT | -6.2% | -28.1% | -29.4% |

| NIFTY MEDIA | -7.6% | -14.5% | -23.9% |

| NIFTY METAL | -12.6% | -15.6% | -31.7% |

| NIFTY PHARMA | -3.5% | -14.6% | -18.6% |

| NIFTY REALTY | -6.4% | -20.4% | -31.3% |

Source: Accord Fintech

Global markets were volatile through June, with a downside bias. The short-lived relief rallies in equities (“dead cat bounce”) did not lead to a sustained recovery in equities. The Dow and FTSE 100 were down by 5%, while the Stoxx Europe 600 Index was battered by 8%. The war situation is still very complex, despite military assistance for Ukraine and an array of economic sanctions against Russia. Ukrainian troops were forced to withdraw from their last battlefront in Luhansk, and it appears that Russia is now on point to control the Donbas region (Mariupol, Donetsk, and Luhansk) – a strategic priority since Russia’s defeat in taking over Kiev.

The immediate effect of war-induced sanctions has been trickling its way throughout Europe since the onset of bans on Russian oil and gas. Headline inflation in Spain breached the 10% mark in June – a level last seen in 1985 – while core inflation stood at 5.5% making Spain yet another European country with multi-decadal high inflation[1]. This is another catalyst that prompted the ECB to increase its interest rates for the first time in 11 years. Meanwhile, Électricité de France (EDF), the nuclear powerhouse of Europe, has hit a 30-year low in nuclear energy output and now France is likely to follow Germany in restarting its coal-powered plants to sustain energy demand. The squeeze has led to French energy giants’ calls for French citizens to reduce their use of petrol, oil, electricity, and gas to ensure sufficient energy supply in winter. On the other side of the English Channel, Britons face a spell of slowing consumer spending due to general increases in the cost of living. A report by KPMG estimates that despite enjoying 7.2% GDP growth in 2021, UK will grow by 3.2% in 2022 and a meagre 0.7% in CY2023[2], highlighting the effect of weak consumer sentiment. It is likely that this effect of slowing demand will continue to be the norm in Europe as the ECB starts being hawkish.

It also appears that grey clouds have dawned upon the US economy. Target alerted investors that their operating margins for 2Q 2022 are likely to shrink from their previous estimate of 5.3% to 2.0%, since it expects the US consumer to have less average disposable income, due to rising energy and food prices. Additionally, Target is now going to focus on items like food and beverages, household essentials, and beauty over their discretionary goods segments. Walmart also claims that families are spending less on discretionary items relative to essentials.

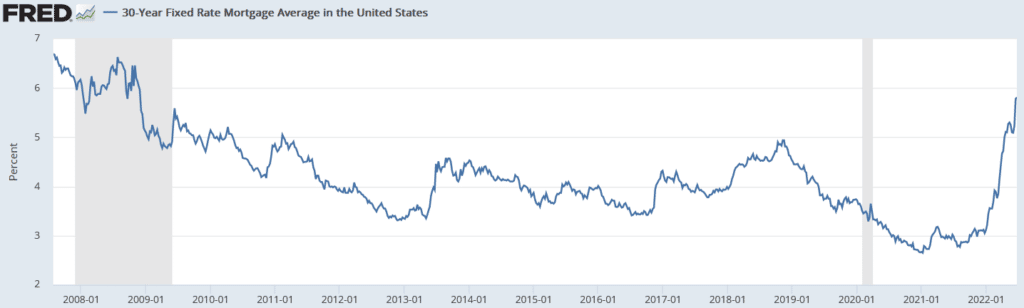

The US housing market is also showing signs of a reversal. Data from FRED shows that the median house price (by sale value) in US increased 16% yoy in 1Q 2022. Over the same period, the fixed-rate 30-year mortgage rate has increased from approximately 3% to approximately 5% (5.8% as on June 23).

Spike in US mortgage rates (shaded areas indicate US recessions)

On the other side of the equation, the proxy for housing supply has shown a sudden spike from Jan 2022 to June 2022. This suggests that since the start of 2022, housing demand has dropped relative to supply, and this can be attributed to the booming prices coupled with the increased borrowing cost in a rising rate environment. The oversupply can cause a negative demand shock for US housing construction inputs in the near term – for instance, lumber prices are already down 45% YTD, erasing the 35% gain observed in 2021.

South-East Asian markets have held relatively strong compared to their Western counterparts – the Hang Seng Index was flat at close at 1%, while the Shanghai Composite surged 5% in June. Dollar flows into Chinese equities were strong in June – BlackRock’s iShares MSCI China ETF saw US$333m inflow on June 29, marking its largest single-day inflow since inception in 2011 – we believe that some of the outflows from India are now being recycled into China, reversing the market flows of 2021. Although the Evergrande debt crisis, and subsequent other developer defaults, are a huge overhang over the Chinese construction and banking sectors, global investors may have piled in now due to the prospect of lockdown restrictions easing and a restart of the Shanghai economy.

Ebbs and Flows of the Dollar

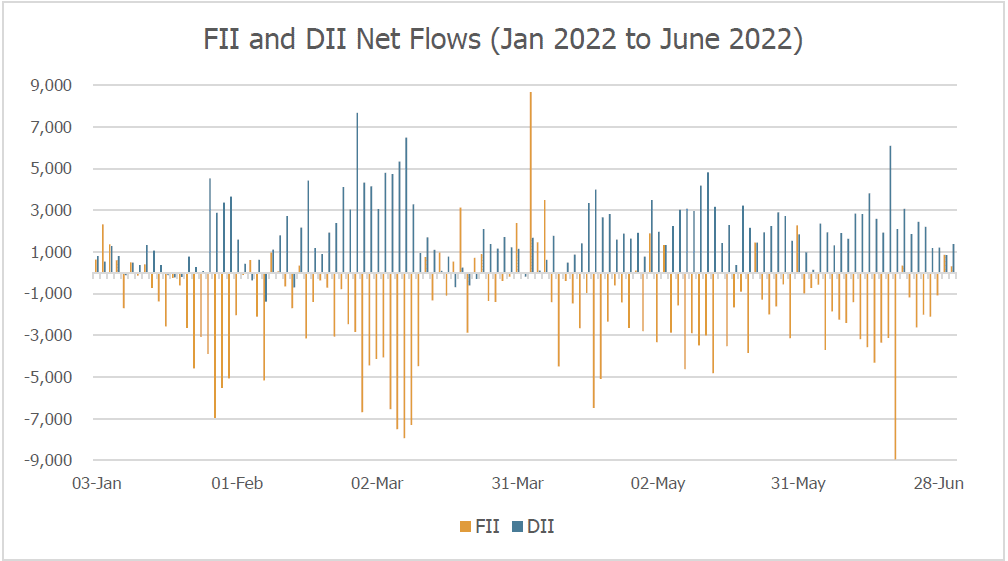

While we track monthly FII and DII flows in equity markets, we have also observed that foreign flows outside of the listed space show a higher-level view of inflows and remittances. Here is a roundup of equity market, FDI, and LRS flows.

FII and DII flows are counter balancing in 2022

FIIs continued to sell Indian equities in June, ~ Rs47,880 crore – their largest net sell-off in 2022. The Rupee has weakened against the US$ by more than 2% since the Fed starting increasing interest rates in March, and the US$-INR rate now stands at an all-time low of INR/US$ 79 levels. Further, the differential in the Fed Funds Rate and the RBI repo rate is now 340 bps (down from 375 bps before the rate tightening). Strength in the greenback has also led to depreciation of the Yuan.

DIIs continue to counterbalance, but their buying momentum is slowing down. The net inflow of Rs46,598 crores is the second instance in 2022 (the first being in March) where DII net purchases have not matched up to FII net selling. As per latest AMFI data, Mutual Funds collected Rs12,286 crores from SIP collections in May. This marks a monthly increase of 3.5% and an annual increase of 39%. A strong SIP order book with good momentum since a year is indicative of the retail investor’s strength.

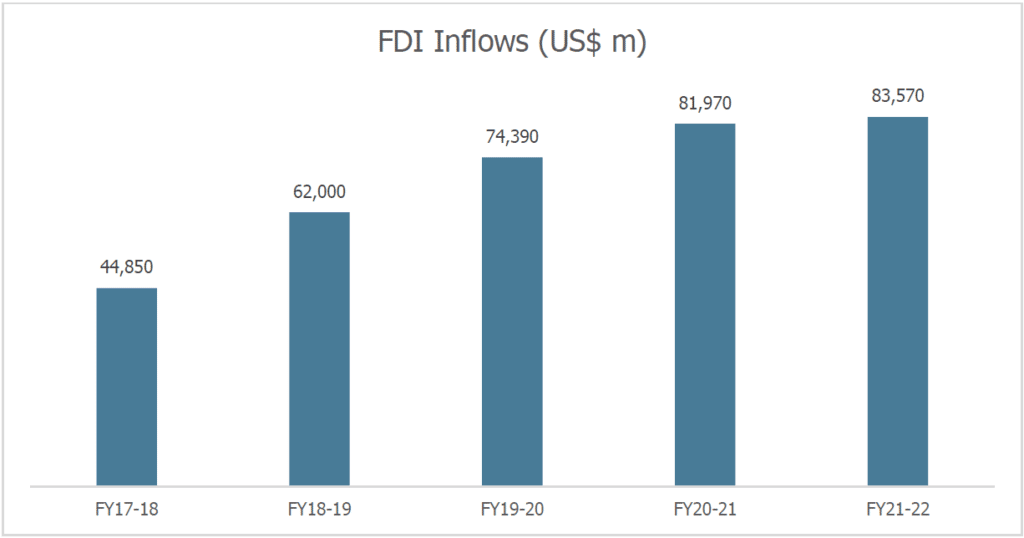

FDI inflows remain steady

According to the Ministry of Commerce and Industry, FDI inflows have increased 20-fold in the last 20 years, with a significant record high of US$83.6bn in FY22. The post-pandemic influx has been particularly interesting – Indian start-ups received US$10.8b from January 2021 to June 2021 alone, with almost half of the funding concentrated in fintech, enterprise tech and edtech[3]. Additionally, the Indian start-up ecosystem has created close to 6.5 lac jobs since 2016, and FDI investment will remain a key variable in supporting this growth. The capital-thirsty, early-stage companies require stable foreign flows to ensure longevity, given that most Indian start-ups fail within the first five years[4].

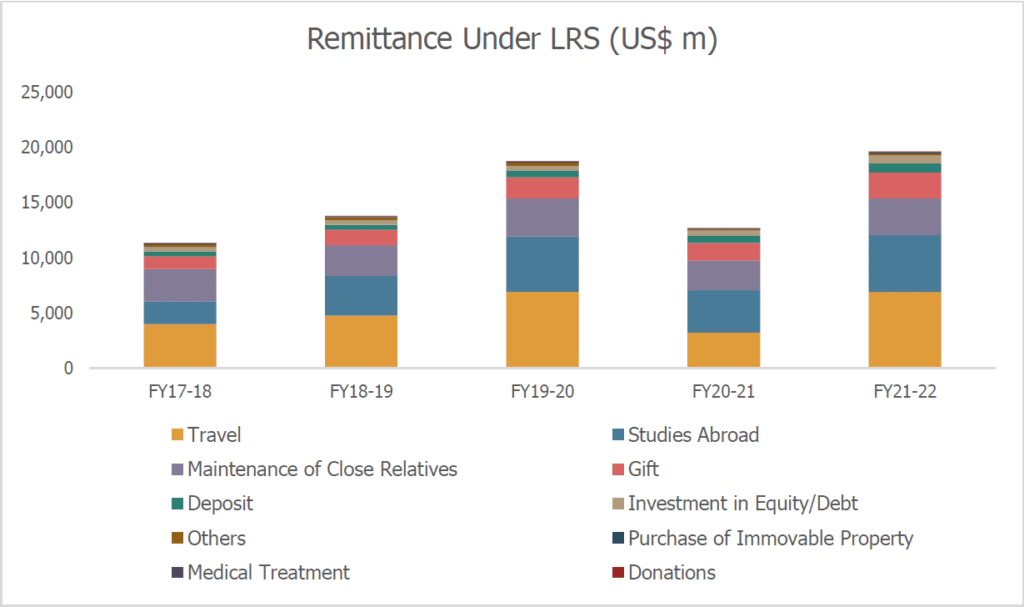

LRS outflows have been steadily increasing

On the other side of dollar flows are resident individuals who send money out of the country via the Liberalised Remittance Scheme (“LRS”). The RBI estimates that outward remittances increased to US$19.6bn in FY22, higher by 55% yoy. Across the 10 different categories, Investments in Equity and Debt and Deposits have witnessed the strongest 3-year uptrend, while remittances for Travel, Studies Abroad, and Gifts have seen the strongest recovery in FY22, in terms of value.

Commodity prices are now signalling a global recession

While we have witnessed a broad-based rally in commodity prices on a year-on-year basis, many key industrial and agricultural commodities have cooled off since peak levels. In the following charts we look at the run up in commodity prices since January 2019, and their subsequent fall from peak levels.

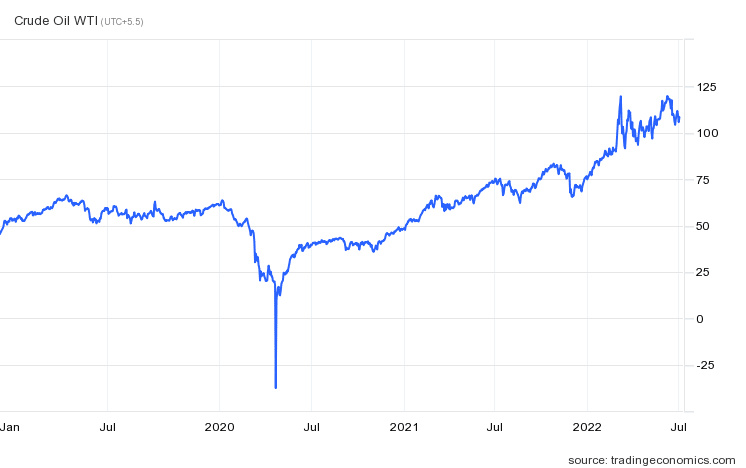

Crude Oil

Crude oil has seen a sharp rise since Russia began its Ukraine war – its price is up 37% since the start of the year, and it is one of the few commodities that is holding at highs due to supply disruptions and sanctions on Russian oil and gas. This has eroded the growth potential of emerging markets in 2022, due to higher import bills, and it is likely that relief will be seen only if oil falls below US$80/bbl.

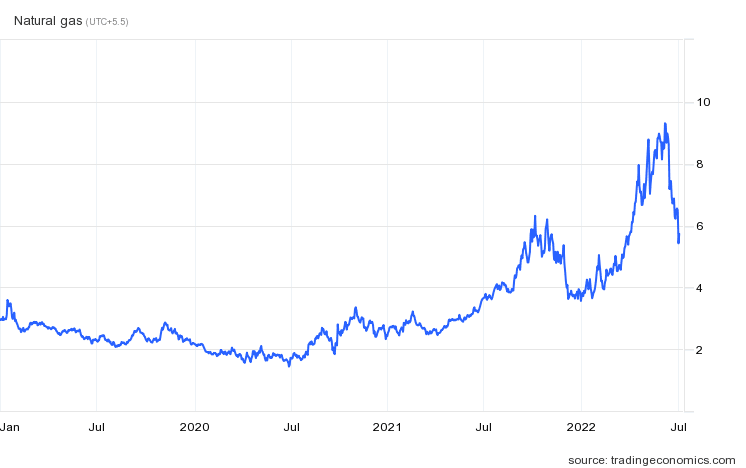

Natural Gas

With similar causes as crude oil price increases, natural gas prices ran up 165% since the start of 2022 till its peak in June 2022. Germany has been forced to re-open its coal-fired power plants after Chancellor Olaf Scholz put restrictions on Russian gas imports. Despite the 38% drop since peak, the decade-high gas prices have sparked an energy crisis in Europe.

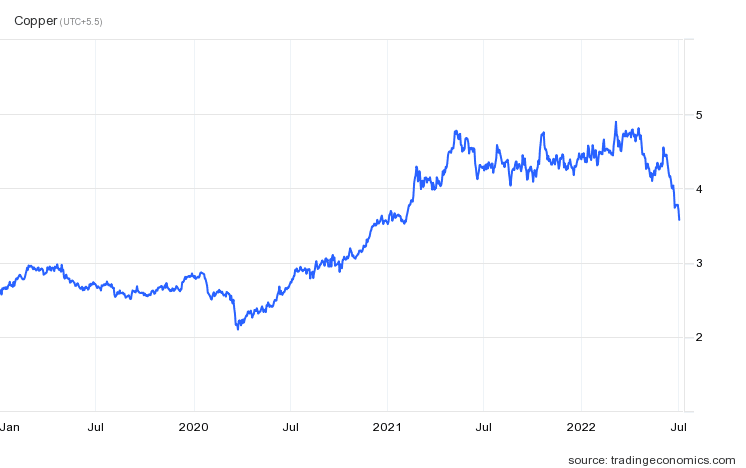

Copper

Dr Copper, the industrial metal that tells us about the health of the global economy, has fallen 27% since peaking in March 2022. This is a sign that industrial demand has been slowing down and may confirm ratings agencies’ downgrades of the growth of the global economy.

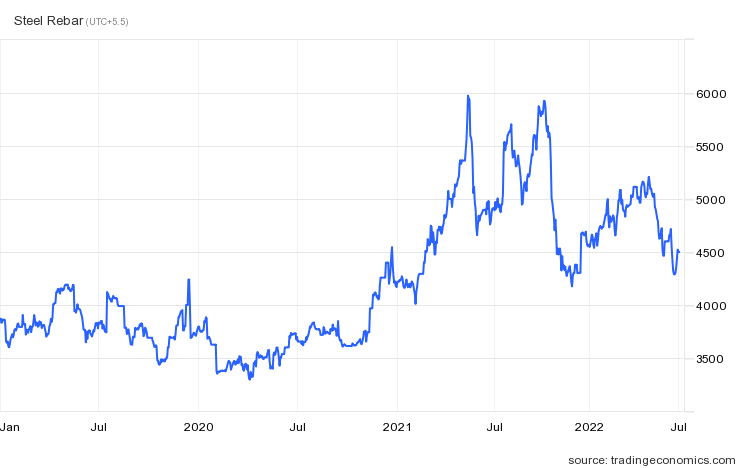

Steel

Prices of steel rebar – or reinforcing steel bar – that has various uses in construction peaked in late 2021 and have fallen by 24% since then. The recent decline of 13% since May 2022 is a sign of weakening demand in China. The lockdowns due to the latest Covid wave in China has resulted in oversupply relative to demand.

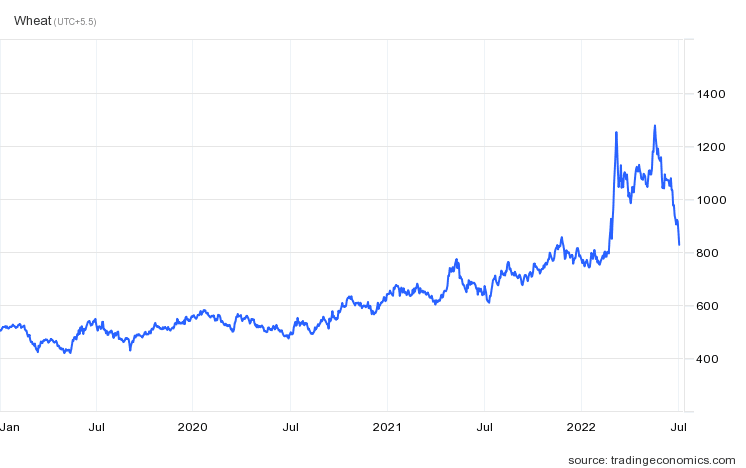

Wheat

A key price point for India’s rural economy, global wheat prices have come off by 35% since the peak in May 2022. Russia and Ukraine are in the top 5 countries that export wheat. Supply chains have been disrupted since March, prices have soared, and food security has been a concern even in Europe. However, the key impact of high wheat prices, and unavailability, will be felt in Africa.

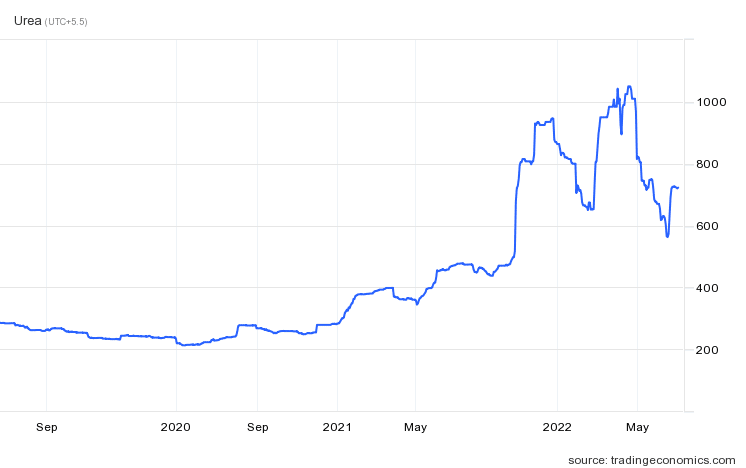

Urea

Urea is another key agricultural commodity that has observed a 30% drop in price since peak after witnessing a 171% run up from April 2021 to April 2022. While it is still high from a historical perspective, the reduction in price of the agricultural input may bring relief to chemical stocks and farmers alike.

The confluence of the recent fall in commodity prices bodes well for importers like India. While it indicates that inflation may not accelerate in the subsequent quarters as it has before, it is not certain whether the worst of inflation is behind us. The asset price inflation due to excess printing is still very much present in the financial system. Further, it is also likely that the fall in prices is more due to demand destruction rather than a healthy regrouping of the global economy. This scenario threatens global economic growth, thereby squeezing central banks between risking persistently high inflation or a recession induced via continual rate hikes.

Ekam Recommendations

Since 2Q 2020, the US Federal Reserve has essentially maintained a mandate to encourage full employment and support the US economy in the wake of a sudden health crisis. This led to interest rates being suppressed at record lows, and it became the status quo for global Central Banks. The tide has now turned. We are seeing a shift of policy from full employment to price stability in the face of rampant inflation.

From a market perspective, the immediate effect will be felt on debt instruments in the form of mark to market losses. Therefore, we continue to recommend that investors re-allocate their fixed-income holdings from debt funds to fixed-coupon bonds.

Indian equities, too, will face pressure due to falling valuations (given that fundamental growth does not compensate for the rise in rates) and potentially sustained FII selling. Highly levered companies with high valuations are likely to be hammered and so it is extremely important to use the volatility to build high-quality portfolios.

We therefore recommend that investors stick to PMS managers who have seen different economic cycles and have a track record of coming out of the volatility with ease. For mutual fund investors, we continue to hold our positive bias on Dividend Yield Funds and Flexi Cap funds via the SIP route.

Gold should also continue to be 10-20% of an investor’s portfolio (and on the higher end for more conservative investors) due to its empirical property of being a store of value. For instance, the Nifty 50 and S&P 500 have fallen by 9% and 20%, respectively, since January 2022 while Gold has held flat at ~ US$1,800/ounce with a high of US$2,053/ounce, immediately after Russia’s attack on Ukraine.

Disclaimer

The data, tables, graphs, and all other depictions are provided by Accord Fintech Private Limited, unless mentioned otherwise on or below the depiction. ATREYI FINANCIAL SERVICES PRIVATE LIMITED is not liable or accountable for accuracy of the data provided in this document.

This document is provided for informational purposes only and it is for the intended recipients only as transmitted by way of printed, electronic, or other media and is not intended as an offer to sell or solicitation of an offer to buy securities or other instruments.

The information contained herein is based on our assumptions, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us, or which was otherwise reviewed by us and can be changed without any prior intimation. This information must not alone be taken as the basis for an investment decision. Please consult your financial, legal and/or tax advisors.

Investment in securities is risky and there is no assurance of returns or preservation of capital. Neither ATREYI FINANCIAL SERVICES PRIVATE LIMITED, nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost capital, lost revenue or lost profits that may arise from or in connection with the use of this information.

Any investment in any product described in this Presentation will be accepted solely on the basis of the offering entity’s constitutional documents, accordingly, this presentation will not form the basis of, and should not be relied upon in connection with any subsequent investment in the fund/ security.

ATREYI FINANCIAL SERVICES PRIVATE LIMITED does not accept any responsibility for any errors whether caused by negligence or otherwise or for any loss or damage incurred by anyone in reliance on anything set out in this Document.

Any person/s accessing data contained in this presentation, hereby confirms that they are not a U.S. person, in accordance with the definition of the term “US Person” under relevant US Securities laws.

No part of this material may be copied or duplicated or redistributed without prior written consent.

Mutual Funds are subject to Market Risks; please invest after seeing the Offer Documents.

[1] Spain Inflation (Source: Reuters)

[3] https://inc42.com/datalab/funding-in-indian-startups-reaches-historical-high-in-h1-2021/

[4] https://www2.deloitte.com/content/dam/Deloitte/in/Documents/finance/in-fa-India%27s-FDI-Opportunity-Deloitte-survey-report-noexp.pdf