Equity Markets Recover in March

While global tensions remain exacerbated, equity markets seem to be pricing in the current situation of the Russia-Ukraine war. Unless Russia escalates the situation by the use of chemical or tactical nuclear weapons, the current situation is a brutal stalemate, with Russia continuing to inflict civilian casualties, but unable to achieve its major military objectives. More military supplies from NATO countries to Ukraine will make Russia’s position even more untenable from a military perspective – its retreat from Kiev to securing its position in the south and east of Ukraine may be reflective of this new reality. We had considered this as probable Option One Endgame in the note we had published previously on the Russia-Ukraine War.

Western countries have aggressively weaponised economic and financial sanctions on Russia, causing shockwaves in prices of key Russian exports like oil and gas. The immediate effect was crude oil surging beyond its 10-year high at US$128/bbl, before settling at US$101/bbl towards the end of the month. This is a key risk for emerging economies and net oil importers. The other issue, the adverse impact of which could be felt largely by African countries, is rising food prices particularly for wheat and corn.

For India, the key supply chain issue is likely to be fertilisers imports being adversely affected. We expect the economic shock from higher oil prices to be limited to a maximum of two quarters, as GCC increases production and the likelihood of Iran and Venezuela re-entering global markets. Hence, we expect crude oil prices to subside to ~$70/bbl again over the next six months.

Domestic equities staged a broad-based recovery in March after taking a beating in February. Although all sectors except Metals are in the red year-to-date, IT and Pharma proved to be solid defensive sectors in March. Mid-cap and small-cap indices posting higher returns than its large-cap counterpart is a positive indicator for a recovering, albeit volatile Indian equity market.

| Index | March Return | YTD Return | Return Since 52-wk high |

| NIFTY 50 | 4.0% | -0.9% | -6.1% |

| NIFTY MIDCAP 100 | 5.2% | -3.6% | -10.7% |

| NIFTY SMALLCAP 100 | 6.0% | -8.6% | -13.4% |

| NIFTY BANK | 0.5% | -0.1% | -13.0% |

| NIFTY AUTO | -2.5% | -5.1% | -13.1% |

| NIFTY FMCG | 2.2% | -3.5% | -13.6% |

| NIFTY IT | 7.3% | -7.2% | -7.9% |

| NIFTY MEDIA | 18.4% | 5.7% | -4.6% |

| NIFTY METAL | 8.9% | 14.1% | -2.9% |

| NIFTY PHARMA | 5.1% | -4.0% | -9.1% |

| NIFTY REALTY | 6.2% | -5.3% | -17.4% |

Global markets continued to follow the developments of the Russia-Ukraine war, as the S&P 500 VIX reached a 1-yr peak at the start of the month before markets settled down gradually. Gold prices also settled down after touching multi-year highs, signalling relative stability in global equities in March, compared with February.

The US Federal Reserve increased interest rates by 25 bps, marking the first increase of interest rates since 2018. Although inflation at 7.9% does no favours for real economic growth, FED Chief Jerome Powell remains confident on the resilience of the US economy, on the back of extremely positive payroll data. The FED also said that it intends to raise rates up to 1.5%, in graduated steps – it intends to take five rate increases of 25bps each. Further, in recent commentary, it said that it could take a rate hike of 50bps as a pre-emptive strike against inflation becoming ingrained.

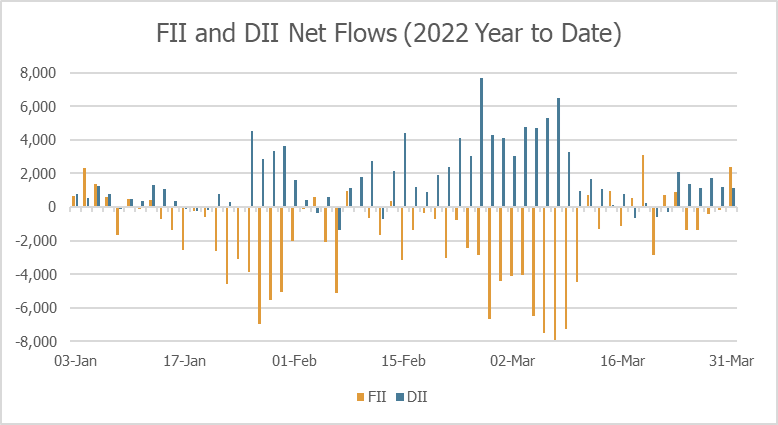

The Great FII Selloff

The FII selloff continued in March, to the tune of Rs41,123cr (US$5.4bn) – this is the highest monthly selloff since March 2020 (Rs61,973cr, US$8.3bn) – taking the YTD total selloff to Rs1,10,019cr (US$14.7bn)! While a selloff due to FED’s actions in terms of balance sheet tapering and rate hikes was warranted, the Russia-Ukraine crisis increased equity risk premiums and accelerated this equity market selloff by FIIs.

A large part of this FII selling can be attributed to risk-off behaviour as observed in other emerging markets. For instance, the MSCI Emerging Markets Index fell by 3.1%, while the MSCI World Index was up by 4.1% in March. A key reason for this is the sharp rise in crude oil prices. These prices could sustain until global supply increases and the Russia-Ukraine situation reaches a resolution. In turn, this will continue to put pressure on current account balances of oil importers at a country level and on gross margins at a company level, especially where crude linked commodities are a key input.

However, one can see from the chart below that FII selling started to taper off in the second half of March.

DIIs have taken this opportunity to increase their positions in Indian equities, with net purchases of Rs39,677cr (US$5.3bn) in March. The YTD tally of Rs1,03,690cr (US$13.8bn) has just about been an adequate counterweight to keep markets up.

Global Sanctions are pummeling Russia

The West has essentially given Russia a timeout on most of their economy for their brutal attack on Ukraine. The use of sanctions as economic warfare dates back to World War I in modern history, when UK and France aimed to shut out Germany and its allies. It is reasonable to say that sanctions in today’s time have far stronger adverse effects in our more interconnected global economy, and especially when practically all developed nations stack up against one economy.

The US, EU and UK have collectively placed sanctions and asset freezes on over 1,000 Russian individuals, including Russian President, Vladimir Putin and Russia’s Foreign Minister, Sergei Lavrov. Financial sector sanctions[1] have included prohibition of securities traded by Russian banks, a ban on individuals and entities to access their bank deposits, and an exclusion of Russian banks from the SWIFT system, thereby disabling Russia’s international trade.

The hardest hitting sanction, which has been used for the first time by the US, EU and UK, was to freeze all the assets of the Russian Central Bank, held in these domiciles. This effectively nullified the war chest that had been built up by the Bank of Russia, and was something completely unanticipated by Russia, in our opinion.

The German Chancellor, Olaf Scholz, asserted his support for Ukraine, and plans to act as a “security guarantor” for the besieged nation[2], although this does not promise military security. In response to Putin’s demand for energy payments in Rouble (rather than Euros or Dollars), Scholz declared that Germany will not be strongarmed into meeting such demands, despite Germany importing over 50% of its natural gas from Russia.

Stopping/sanctioning European imports of Russian oil and gas is critical to enacting a complete freeze of the Russian economy by the Western world – currently, the oil and gas imports by EU are still funding the Russian war effort in Ukraine. While both France and Germany have now said that they will be cutting back on Russian imports, finding substitutes will take time. The previous German policy of cutting back on nuclear power, and shutting nuclear power stations progressively, has also led to the current German dependence on Russian oil. France is better placed on this score as it has been increasing its nuclear power plants. However, for an embargo on Russian oil and gas, these two EU heavyweights have to work in tandem.

The shut out of Russian individuals, financial institutions, and goods and services from the global economy was not taken lightly by the Putin administration. The Bank of Russia intervened in forex markets for the first time since 2014 (Crimea annexation) to prop up the Rouble – although Russia’s forex reserves are at an all-time high, a majority of the reserves are parked outside of Russia, making it practically impossible to use these funds due to the financial sanctions by the US and EU. In an additional move to save the Rouble and to prevent a domestic bank run, the Bank of Russia increased rates to ~20% on domestic deposits.

The Bank of Russia also shut down the Moscow Stock Exchange for over three weeks, and banned all selling by foreign entities when it reopened. It also banned short selling and trading was limited to a small section of stocks.

Finally, the Bank of Russia attempted to peg the Rouble to Gold, by saying it will sell Gold at an equivalent rate of US$1,600/oz., which was a 17% discount to the market price as of 31st March. This attempt is unlikely to work because global banks are prohibited from dealing with Russian banks, and any other entity that attempts to buy Gold from Russia would face secondary sanctions from the US and EU.

However, the Rouble has regained practically all its losses against the US Dollar, post the Ukraine invasion and is now trading at nearly its pre-invasion levels – in our view, this is an illusion because the Rouble is not freely convertible, and the Bank of Russia has imposed multiple restrictions on foreigners’ ability to sell Russian assets. We will know the true level of the Rouble only at the end of the war and the removal of restrictions on foreign investors, and possibly only after Russia re-joins global trade.

In terms of war strategy, we had mentioned in our February note on the Russia-Ukraine war that the endgame could take two potential shapes – a partioning of Ukraine versus a total takeover. Russia chose the latter, but this has not worked out well for Russia. Ground-level reports indicate that ~10% of Russian troops have been killed and are now disobeying orders in some cases – there was a report of a Colonel of a motorised battalion group being killed by his own troops. This is a sign of the low morale in the Russian camp while the Ukrainians continue to defend their cities.

The latest reports in April show that Russia is pulling back troops from the Kiev region in Northern Ukraine to Belarus, and looking to consolidate its hold in the South and East of Ukraine – this was our Option One endgame. But, even here, Ukrainians continue to fight and hold on to their cities, despite indiscriminate bombing by the Russians, leading to complete destruction of some cities and significant civilian casualties. Russia has also not been able to establish a land bridge yet from Crimea to Russia, which was supposed to a war aim for Russia.

The western countries, specifically the US, have not been pleased with India remaining “neutral” about the war. India’s crude oil imports from Russia account for 1.5% of total imports. However, Russia has been a major arms and related equipment supplier to India – ~70% of India’s defence imports are still from Russia. And, this has been the key dilemma for India. The US has given India some space on this issue because it sees India as a key ally against China, and India has also pushed back against EU nations who asked India not to buy Russian oil by pointing at their own imports. India is currently walking a fine line, but the current revelations about Russian atrocities will put India in a tighter position, and it may have to take a stronger position soon.

Disclaimer

The data, tables, graphs, and all other depictions are provided by Accord Fintech Private Limited, unless mentioned otherwise on or below the depiction. ATREYI FINANCIAL SERVICES PRIVATE LIMITED is not liable or accountable for accuracy of the data provided in this document.

This document is provided for informational purposes only and it is for the intended recipients only as transmitted by way of printed, electronic, or other media and is not intended as an offer to sell or solicitation of an offer to buy securities or other instruments.

The information contained herein is based on our assumptions, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us, or which was otherwise reviewed by us and can be changed without any prior intimation. This information must not alone be taken as the basis for an investment decision. Please consult your financial, legal and/or tax advisors.

Investment in securities is risky and there is no assurance of returns or preservation of capital. Neither ATREYI FINANCIAL SERVICES PRIVATE LIMITED, nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost capital, lost revenue or lost profits that may arise from or in connection with the use of this information.

Any investment in any product described in this Presentation will be accepted solely on the basis of the offering entity’s constitutional documents, accordingly, this presentation will not form the basis of, and should not be relied upon in connection with any subsequent investment in the fund/ security.

ATREYI FINANCIAL SERVICES PRIVATE LIMITED does not accept any responsibility for any errors whether caused by negligence or otherwise or for any loss or damage incurred by anyone in reliance on anything set out in this Document.

Any person/s accessing data contained in this presentation, hereby confirms that they are not a U.S. person, in accordance with the definition of the term “US Person” under relevant US Securities laws.

No part of this material may be copied or duplicated or redistributed without prior written consent.

Mutual Funds are subject to Market Risks; please invest after seeing the Offer Documents.

[1] https://ec.europa.eu/info/strategy/priorities-2019-2024/stronger-europe-world/eu-solidarity-ukraine/eu-sanctions-against-russia-following-invasion-ukraine_e

[2] https://www.reuters.com/world/europe/scholz-zelenskiy-germany-ready-act-security-guarantor-ukraine-2022-03-30/